The issue: Consumers shocked by charges they question or couldn’t avoid

Jeani Brinson didn’t have insurance when she sought care at a California hospital emergency room a few years ago.

Knowing she would pay every charge out of pocket, Brinson had extra incentive to comb through the bill she received once she returned home.

Her story, shared on the Voices for Affordable Health Facebook page, shows how important it is for consumers to scrutinize their health care bills.

“I called the hospital,” Brinson says, “because we were being charged for two things that I absolutely knew had not been used for me. A cannula for oxygen and a prenatal monitor.”

The hospital refused to adjust the charges, and Brinson’s next call was with the collections office.

“I explained that I had been trying to deal with the hospital to no avail,” she says. “When I told her that I was 64 years old and not had any prenatal monitoring or oxygen, she left me on the line while she contacted the hospital. She came back on – subtracted those charges, and I sent the check that day.”

While Brinson’s story ended well, it also reflects the anger and frustration consumers often feel when they receive hospital or doctors’ bills that are unexpectedly high or difficult to understand.

“Surprises” on medical bills are sometimes just incorrect. Others occur when patients did not realize how much their lab work, imaging tests or other treatments would cost them out-of-pocket.

Another form of surprise billing — also known as “balance billing” — occurs when there’s a difference between what your insurance company has agreed to pay a hospital or physician vs. the higher amounts charged by providers who have no agreement with the insurer.

Patients often have no notice or choice when receiving treatment. They wake up from surgery only to learn that the anesthesiologist did not belong to their insurance company’s network. Other common out-of-network providers: radiologists who look at a scan and pathologists who examined tissue samples. Critics call these “hidden providers.”

Even after a patient’s insurance company has paid the out-of-network provider what is determined to be a fair rate, the patient remains liable for the extra and unexpected charges.

“The problem is, you don’t just get one bill. You get three or more and can only hope the physicians used are in your network since you are not told this at the time they provide services,” Karin Kimbrough of Bothell, Wash., posted on the Voices Facebook page.

Monica Pursley also posted: “Radiologists to read the imaging, ER doctors, specialists … issues you are too sick to care about until you get the bills and find out two-thirds of the services were not contracted with your health insurance… If you’re lucky enough to have health insurance.”

Danna Hall of Covington, Wash., posted: “I wasn’t expecting separate bills for the ER doctor on top of the ER care.”

Emergency room visits are often cited as the most common and egregious example of surprise bills.

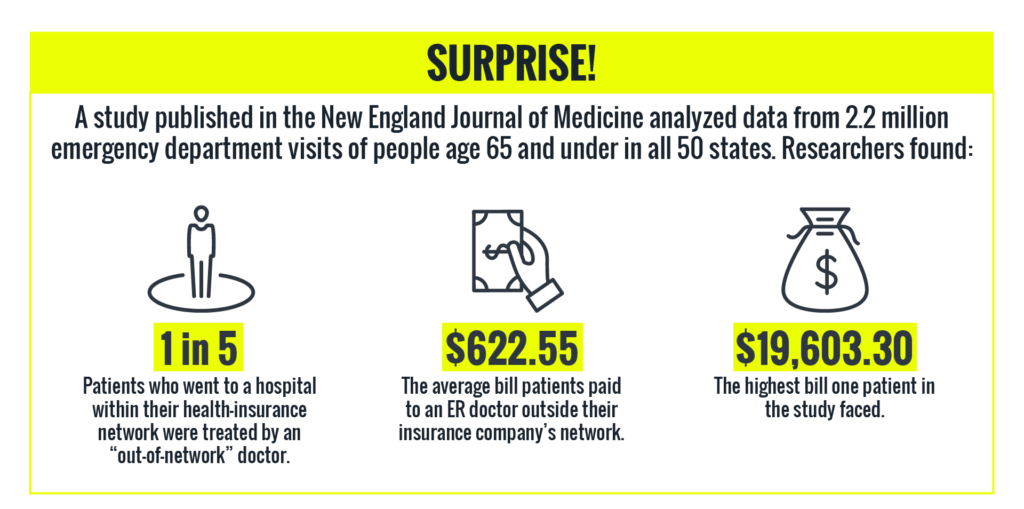

A study published in the November 2016 New England Journal of Medicine found that patients in all 50 states were hit with big “out-of-network” ER bills. Even though these patients had sought care from a hospital within their insurance network, the doctors who treated them were independent contractors and not subject to the negotiated rates.

Yale University researchers analyzed 2.2 million emergency visits nationwide between January 2014 and September 2015. They found that 22 percent of the people who went to emergency departments within their health insurance networks were unknowingly treated by an out-of-network doctor. As a result, patients and their families were liable for hundreds, sometimes thousands, of dollars. In some cases, out-of-network ER doctors charged 798 percent of the Medicare allowed rate.

“This is just wrong and we must do better,” Zack Cooper, an assistant professor at the Yale School of Public Health and one of the study’s authors, said in a press release. “People should not face financial ruin from medical bills they cannot reasonably avoid.”

Separate research by the Federal Trade Commission reached similar conclusions. FTC economists and researchers examined data from multiple private insurers from 2007 to 2014. Their report, published in Health Affairs found:

- 20 percent of hospital patients admitted following an emergency room visit received an unexpected bill.

- Patients scheduled for planned, elective procedures were still vulnerable to unexpected charges.

- The sicker a patient was, the more likely he or she was to get a surprise medical bill.

“It’s clearly a consumer protection issue,” Christopher Garmon, an FTC economist, told Voices for Affordable Health.

The solution: Legislators look at legal protections; urge consumers to speak out

While the Yale researchers found “virtually no federal protections against surprise physician bills,” some elected officials are starting to pay attention to the issue.

In a letter asking the Federal Trade Commission to investigate, U.S. Sen. Bill Nelson, D-Fla., called surprising billing “unfair and deceptive.”

A handful of states, including Oregon and Utah, are debating laws to protect consumers.

Utah State Rep. Jim Dunnigan, R-Taylorsville, has spent the past few years working on a solution to surprise billing.

“It’s a real dog fight,” Dunnigan told Voices for Affordable Health.

At the same time, he says, it’s a fight worth having.

Dunnigan, an insurance agent and co-chairman of the Utah Legislature’s Health Reform Task Force, says doctors and hospitals maintained early on that surprise medical billing wasn’t a problem. Today he says the hospitals, insurance companies and consumer advocates are ready to tackle the issue. Doctors have yet to sign on.

Meanwhile, Dunnigan continues to collect stories from clients or constituents who are saddled with unexpected bills.

“There was a lady who went to a hospital down the street from me and paid her 20 percent,” he says. “The insurer paid 80 percent. And she still got a balance bill that was several thousand dollars.”

While he and other elected officials work on legal protections, Dunnigan advises consumers to speak out.

“Try to negotiate with the hospital and plead your case,” he says. “Get a consumer advocate, perhaps a legislator, and make the community aware. Publicize it. I don’t mean that in a mean-spirited way, just let the rest of the community be aware of what’s going on.”